|

|

|

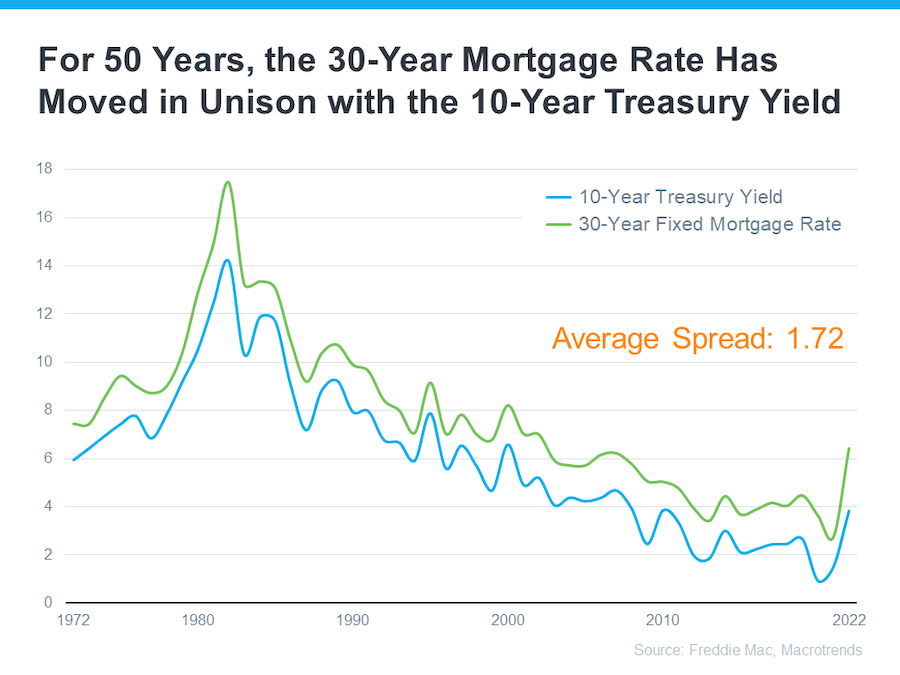

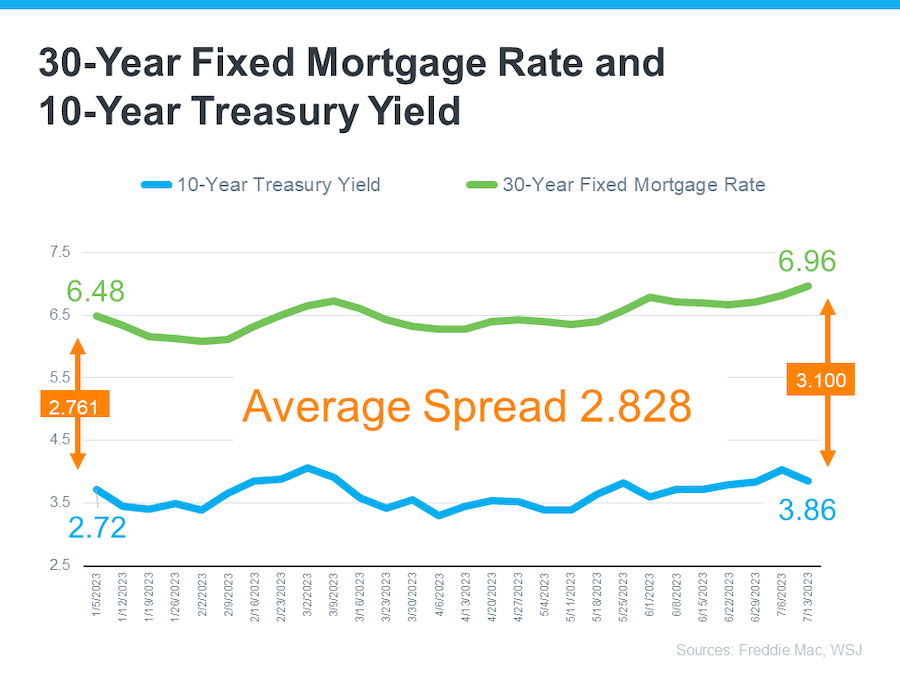

If you are following mortgage rates because you know they impact your borrowing costs, you may be wondering what the future holds for them. Unfortunately, there is no easy way to answer that question because mortgage rates are notoriously hard to forecast. But, there is one thing that is historically a good indicator of what will happen with rates, and that is the relationship between the 30-Year Mortgage Rate and the 10-Year Treasury Yield. Here is a graph showing those two metrics since Freddie Mac started keeping mortgage rate records in 1972:   Why Does This Matter for You? This may feel overly technical and granular, but here is why homebuyers like you should understand the spread. It means, based on the normal historical gap between the two, there’s room for mortgage rates to improve today. And, experts think that is what lies ahead as long as inflation continues to cool. As Odeta Kushi, Deputy Chief Economist at First American, explains: It is reasonable to assume that the spread and, therefore, mortgage rates will retreat in the second half of the year if the Fed takes its foot off the monetary tightening pedal . . . However, it is unlikely that the spread will return to its historical average of 170 basis points, as some risks are here to stay. Similarly, an article from Forbes says: Though housing market watchers expect mortgage rates to remain elevated amid ongoing economic uncertainty and the Federal Reserves rate-hiking war on inflation, they believe rates peaked last fall and will decline to some degree later this year, barring any unforeseen surprises. Bottom Line If you are either a first-time home buyer or a current homeowner thinking of moving into a home that better fits your current needs, keep on top of what is happening with mortgage rates and what experts think will happen in the coming months.

Over $125 Million in Career Sales

|

|

|

|

It is a common misconception that a real estate agent primarily learns of someone looking to buy or sell a home when someone simply calls an agency looking for an agent to help them. Although this can happen, it is very rare. In fact, over 80% of the referrals I receive come from past clients and past coworkers just like you. The other 15-20% of referrals comes from our national network of relocation companies and other Coldwell Banker agencies across the country. The greatest compliment I can receive is when someone like you refers me to a friend, coworker or family member of theirs. If you, or someone you know, are looking to either buy or sell a home then I would certainly appreciate the opportunity to earn your business. Do you know of someone looking to buy or sell a home?  Click the vCard below to download my contact information to load on your phone and to share with anyone you know that would benefit from my help in buying or selling a home.

|

|

|

12401 Old Meridian Street Carmel, In 46032 Email brad@btgough.com Mobile (317) 590-3571 Office (317) 844-1131 Website www.btgough.com |