|

|

|

|

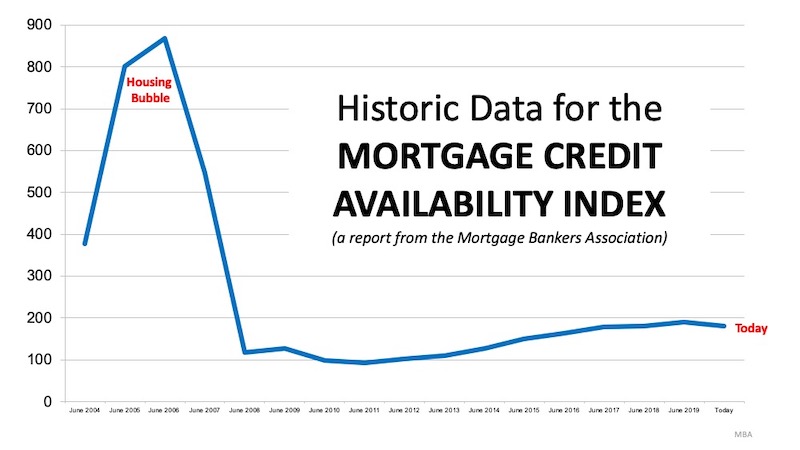

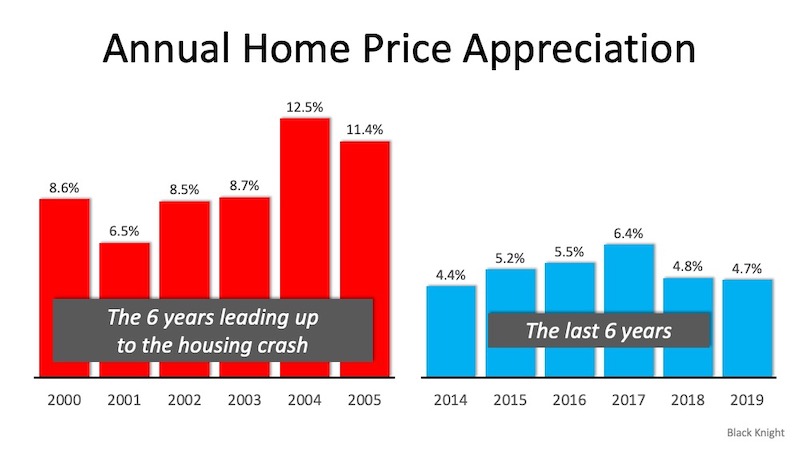

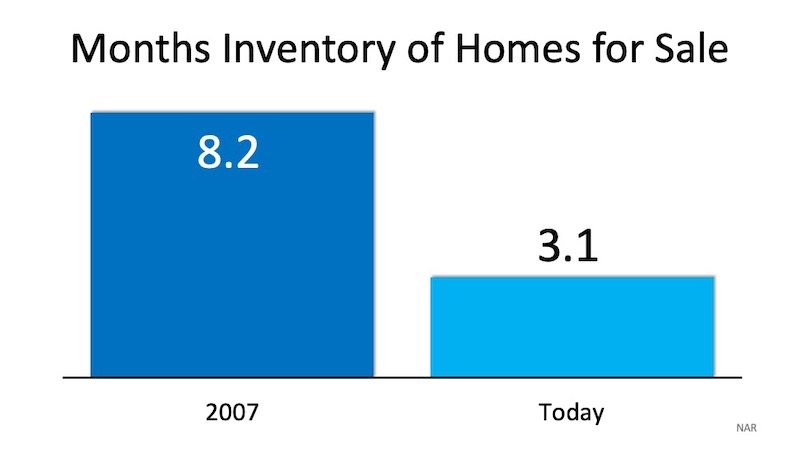

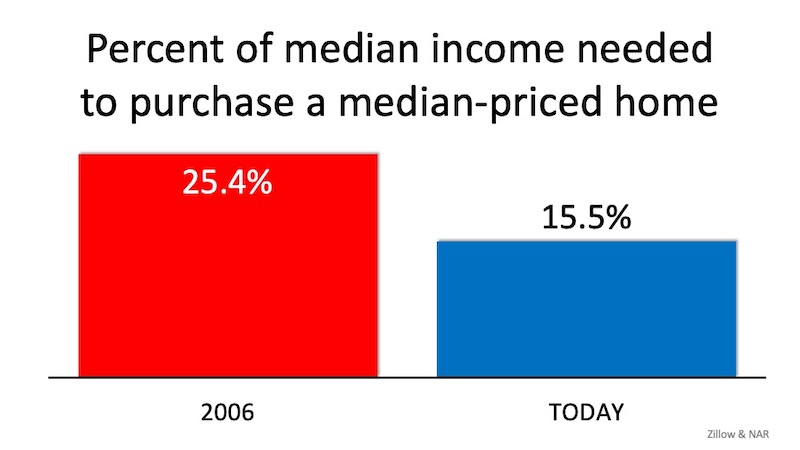

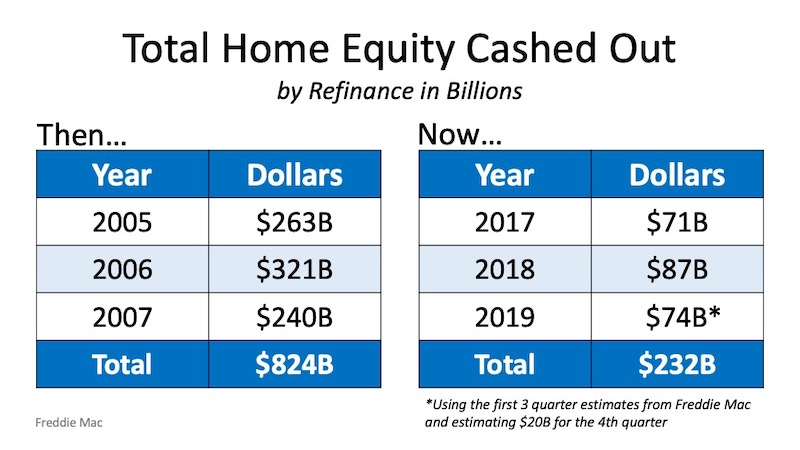

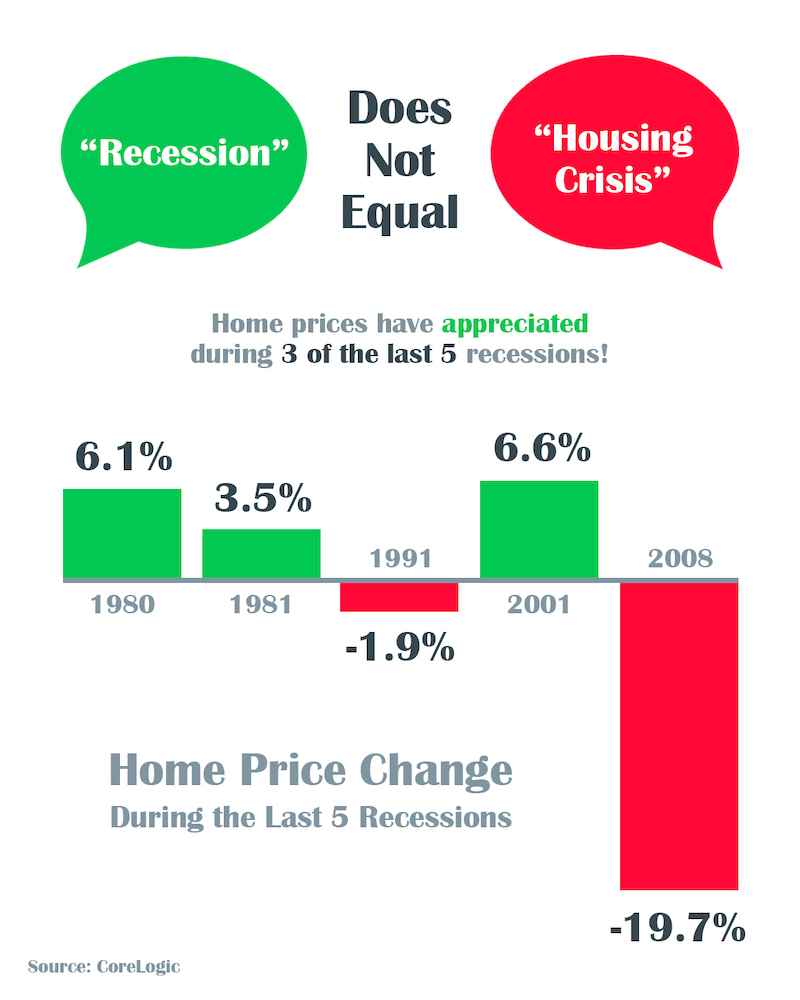

With all of the volatility in the stock market and uncertainty about the Coronavirus (COVID-19), some are concerned we may be headed for another housing crash like the one we experienced from 2006-2008. The feeling is understandable. Ali Wolf, Director of Economic Research at the real estate consulting firm Meyers Research, addressed this point in a recent interview: With people having PTSD from the last time, they are still afraid of buying at the wrong time. There are many reasons, however, indicating this real estate market is nothing like 2008. Here are five visuals to show the dramatic differences. 1. Mortgage standards are nothing like they were back then. During the housing bubble, it was difficult NOT to get a mortgage. Today, it is tough to qualify. The Mortgage Bankers Association releases a Mortgage Credit Availability Index which is a summary measure which indicates the availability of mortgage credit at a point in time. The higher the index, the easier it is to get a mortgage. As shown below, during the housing bubble, the index skyrocketed. Currently, the index shows how getting a mortgage is even more difficult than it was before the bubble.  2. Prices are not soaring out of control. Below is a graph showing annual house appreciation over the past six years, compared to the six years leading up to the height of the housing bubble. Though price appreciation has been quite strong recently, it is nowhere near the rise in prices that preceded the crash.  There is a stark difference between these two periods of time. Normal appreciation is 3.6%, so while current appreciation is higher than the historic norm, it is certainly not accelerating beyond control as it did in the early 2000s. 3. We do not have a surplus of homes on the market. We have a shortage. The months supply of inventory needed to sustain a normal real estate market is approximately six months. Anything more than that is an overabundance and will causes prices to depreciate. Anything less than that is a shortage and will lead to continued appreciation. As the next graph shows, there were too many homes for sale in 2007, and that caused prices to tumble. Today, there is a shortage of inventory which is causing an acceleration in home values.  4. Houses became too expensive to buy. The affordability formula has three components: the price of the home, the wages earned by the purchaser, and the mortgage rate available at the time. Fourteen years ago, prices were high, wages were low, and mortgage rates were over 6%. Today, prices are still high. Wages, however, have increased and the mortgage rate is about 3.5%. That means the average family pays less of their monthly income toward their mortgage payment than they did back then. Here is a graph showing that difference:  5. People are equity rich, not tapped out. In the run-up to the housing bubble, homeowners were using their homes as a personal ATM machine. Many immediately withdrew their equity once it built up, and they learned their lesson in the process. Prices have risen nicely over the last few years, leading to over fifty percent of homes in the country having greater than 50% equity. But owners have not been tapping into it like the last time. Here is a table comparing the equity withdrawal over the last three years compared to 2005, 2006, and 2007. Homeowners have cashed out over $500 billion dollars less than before:  The good news is, home values actually increased in 3 of the last 5 U.S. recessions and decreased by less than 2% in the 4th.  With all of the havoc being caused by COVID-19, many are concerned we may see a new wave of foreclosures. Restaurants, airlines, hotels, and many other industries are furloughing workers or dramatically cutting their hours. Without a job, many homeowners are wondering how they will be able to afford their mortgage payments. In spite of this, there are actually many reasons we will not see a surge in the number of foreclosures like we did during the housing crash over ten years ago. Here are just a few of those reasons: The Government Learned its Lesson the Last Time During the previous housing crash, the government was slow to recognize the challenges homeowners were having and waited too long to grant relief. Today, action is being taken swiftly. Just this week: The Federal Housing Administration indicated it is enacting an immediate foreclosure and eviction moratorium for single family homeowners with FHA-insured mortgages for the next 60 days. The Federal Housing Finance Agency announced it is directing Fannie Mae and Freddie Mac to suspend foreclosures and evictions for at least 60 days. Homeowners Learned their Lesson the Last Time When the housing market was going strong in the early 2000s, homeowners gained a tremendous amount of equity in their homes. Many began to tap into that equity. Some started to use their homes as ATM machines to purchase luxury items like cars, jet-skis, and lavish vacations. When prices dipped, many found themselves in a negative equity situation (where the mortgage was greater than the value of their homes). Some just walked away, leaving the banks with no other option but to foreclose on their properties. Today, the home equity situation in America is vastly different. From 2005-2007, homeowners cashed out $824 billion worth of home equity by refinancing. In the last three years, they cashed out only $232 billion, less than one-third of that amount. That has led to: 37% of homes in America having no mortgage at all Of the remaining 63%, more than 1 in 4 having over 50% equity Even if prices dip (and most experts are not predicting that they will), most homeowners will still have vast amounts of value in their homes and will not walk away from that money. There Will Be Help Available to Individuals and Small Businesses The government is aware of the financial pain this virus has caused and will continue to cause. Yesterday, the Associated Press reported: In a memorandum, Treasury proposed two $250 billion cash infusions to individuals: A first set of checks issued starting April 6, with a second wave in mid-May. The amounts would depend on income and family size. The plan also recommends $300 billion for small businesses. Are you moving soon? Click on the video below for some great ideas for packing to make it easier and more efficient for you.  |

|

|

|

Housing data released by the MIBOR BLC listing service for February 2020 shows: Median sales price $188,490 Average days on market 59 Months of Inventory 1.9 Closed Sales 2,069 Read More |

|

|

|

Existing-Home Sales Down 1.3% in January Despite significant sales declines in the West, overall existing-home sales increased substantially year-over-year. NAR releases national and regional existing-home sales price and volume statistics on or about the 25th of each month. Each report includes data for 12 months and annual totals going back three years. Reports are available for existing single-family homes, condos , and co-ops. Both median and average prices are included. Read More |

|

|

|

Over 93 Million in Sales - Click to View |

|

|

|

It is a common misconception that a real estate agent primarily learns of someone looking to buy or sell a home when someone simply calls an agency looking for an agent to help them. Although this can happen, it is very rare. In fact, over 80% of the referrals I receive come from past clients and past coworkers just like you. The other 15-20% of referrals comes from our national network of relocation companies and other Coldwell Banker agencies across the country. The greatest compliment I can receive is when someone like you refers me to a friend, coworker or family member of theirs. If you, or someone you know, are looking to either buy or sell a home then I would certainly appreciate the opportunity to earn your business. Do you know of someone looking to buy or sell a home?  |

|

|

|

12401 Old Meridian Street Carmel, In 46032 Email brad@btgough.com Mobile (317) 590-3571 Office (317) 844-1131 Website www.btgough.com   |

|

|

|

There are so many great charities out there that and it is very hard to decide what to donate to. My wife Elissa and I have been very fortunate and have a good life. We simply can't donate to everything, however, we are very passionate about several different causes. We are sustaining members for the following organizations and encourage each of you to donate in any way you can to a cause that you are passionate about too.

The American Society for the Prevention of Cruelty to Animals

|

|